As economists, we usually are in favor of free trade. We recognize that free trade offers many benefits to different countries!

Why is free trade a good idea?

-The law of comparative advantage

-When there is regional specialization and trade, the world production of all products rises

-This maximizes the world's average standard of living (world GDP per capita)

On the other hand, some countries may attempt to instill protectionist policies (policies which counteract free trade in order to protect domestic firms from international competition). These can include both TARIFFS and NON TARIFF BARRIERS (NTBs, such as quotas, customs procedures, anti-dumping duties and countervailing duties).

Why might nation choose certain degrees of protectionism?

REASONS WHICH RELATE TO MAXIMIZING NATIONAL INCOME

1: To improve the terms of trade! If a country is large enough, it can force the world price downward for goods it imports by imposing a Tariff

2: Infant Industry Protection. Some countries may set up trade barriers in order to protect domestic firms from international competition, with the hopes that these industries will grow to the point where they can realize economies of scale. The idea here is that under protection, infant industries will eventually "grow up" to the point where they will be able to compete on the international market without need of protectionism. A problem with this is that not all industries develop to this level of competency while under protection. Canada's national policy of 1876 was an example of infant industry protection directed at improving Canadian manufacturing.

3: Learning by doing. This sort of goes along with infant industry protection, but along with protecting developing industries from international competitors, protectionism can also simply give those industries time to operate, which gives personnel time to gain mastery over certain procedures. In this way, countries can turn comparative disadvantages into comparative advantages.

PROBLEM! Not every industry which gets chosen for protection will ultimately grow up to be an international "winner", so each time the government placed an industry under protection, they are effectively gambling (as protectionism exacts economic costs) on their choice. If governments do this frequently, statistically, they are likely to choose more losers than winners, which would be quite costly.

=(

4: Protectionism can allow certain key industries to earn economic profits and thus innovate more. As such, Canada has strategic trade policy in place with regards to Bombardier (if you remember, they're the company which made the olympic torches)

OTHER REASONS

1: There are advantages from diversification. Countries which are only specialized in a narrow range of products may use protectionism in order to diversify their economies (which gives local firms a "safe space" to expand into new industries, thus increasing the range of products produced domestically). This can be useful in that it buffers the volatility and risk posed by price changes and new technologies by spreading production to several different sectors. The idea here is not to "put all of your eggs in one basket" (although, often, this is more of a political argument than an economic argument)

2: Protectionism lets governments protect favored groups! In Canada, competitive advantage favors skilled labour over unskilled labour, and as a result, free trade may lower the wages of unskilled laborers (who are now competing with wage slaves from overseas). Here, protectionism can redistribute income to certain productive groups, but at the expense of the collective standard of GDP. There is a deadweight loss!

USUALLY, HOWEVER, PROTECTIONISM IS FOR POLITICAL OR FALLACIOUS ECONOMIC REASONS!!!!!!!!! >=(

HERE ARE SOME FAULTY ARGUMENTS WHICH PEOPLE WILL OFTEN POSE IN ORDER TO SUPPORT PROTECTIONISM!

1: "We've got to keep our money at home"

The Premise: If I buy a domestic good, by country will have both the good AND the money used to buy that good

Why it's incorrect: Domestic money is only useful for buying domestic goods. If you are buying foreign products, the money you spend on those products eventually gets used to buy Canadian products- it flows between the two trading countries

2: "We've got to protect ourselves from low-cost foreign labour"

The Premise: Low wage foreign goods will eliminate domestic goods from the market, and thus lower the domestic standard of living.

Why it's incorrect: This goes against the law of comparative advantage. Even if a foreign country can produce all goods at a lower cost than Canada, it would still be advantageous to trade, as trade will lower the opportunity cost of having certain products.

3: "Exports are good, and imports are bad"

The Premise: Exports add to domestic GDP, while imports take away from domestic GDP

Why it's incorrect: Standard of living is dependent on consumption, not production. If a country exports a lot of goods, but derives its comparative advantage by paying its workers very low salaries, then those workers will not be able to consume very many products, on average, and thus that country's standard of living will probably be quite low.

4: "Protectionism creates local jobs"

The Premise: Protecting the domestic market can help save local jobs, and thus combat unemployment

Why it's incorrect: Protectionism reduces employment in other sectors which may have local comparative advantages, and thus, while it may increase employment in one sector, the overall economic effect is inefficient.

-----------------

METHODS OF PROTECTIONISM

TARIFFS: Import Duties- these are a tax on imports. They increase costs for domestic consumers, but benefit domestic producers (who can sell at higher than the world price) and the government (who receives tax revenue). Tariffs create a deadweight social loss for the economy as a whole.

Originally, at the world price, Canada will import 1500 units of this product, and domestic producers will supply the other 500 units needed to satisfy demand.

Once the tariff raises the prices, Canada only imports 500 units of the product, and domestic producers supply the other 1000 units needed to satisfy domestic demand (as you can see, demand has decreased due to the higher price).

Consumer lose surplus represented by sections C, D, E, & F due to the Tariff

Producers gain surplus represented by section C due to the Tariff (the increase in price times the increase in production, minus the costs incurred by increasing production)

The government gains section E due to the Tariff (the quantity of foreign imports at the Tariff price, multiplied by the amount of the Tariff)

SECTIONS D & F REPRESENT A DEADWEIGHT SOCIAL LOSS, HOWEVER! (tragic, isn't it!?)

--------------------------------

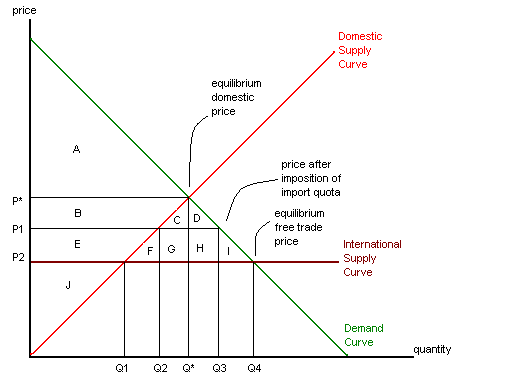

QUOTAS AND VOLUNTARY EXPORT RESTRICTIONS (VERs)

An import quota is like a quantity ceiling- it restricts the quantity of products which a country will import

With a voluntary export restriction, the exporter agrees to limit the amount of exports it will send to any one country.

This incurs costs for domestic consumers, but benefits domestic producers

The net result is a deadweight social loss which is greater than that which results from a Tariff!

At the world price, Canada will import Q4 - Q1, and domestic producers will supply Q1

Let's say that a quota restricts domestic imports to Q3 - Q2. If this happens, then the domestic price must rise to P1, where the quota exactly satisfies the excess demand which domestic producers cannot meet.

Consumers lose surplus equal to E, F, G, H, & I due to the quota,

Producers gain surplus equal to E due to the quota

Since there is no taxation here, the higher price on the quota goods causes foreign producers to gain surplus equal to G & H

THERE IS A DEADWEIGHT LOSS EQUAL TO SECTIONS F & I due to the quota! >=(

Usually, in trade barrier situations, exporters prefer a quota (so they can gain the extra revenue section) while importing governments prefer a tariff (so they can gain the extra revenue section).

----------------------------------------

NON-TARIFF BARRIERS

1: Antidumping Duties

-Dumping is the practice of selling a good in a foreign country at a price below domestic prices at a reason other than costs

-This is like price discrimination (remember from micro) but on an international level

-Usually, it is only temporary, in order to sell off excess supply, or to weaken local industries and force reliance on foreign imports

-It is seen as anti-competitive, and many people believe that it is an unfair form of competition

-Antidumping duties (taxes to bring "dumped" imports back up to the domestic price level) are often used to compensate for this

-Recently, however, these have been abused and used as a non-trade barrier

-When Antidumping Duties are used, the domestic price becomes the price floor, regardless of the foreign price (which can lead to an inflexibility in domestic prices compared to the world price)

-As such, if the world price falls below the average costs for domestic producers, they are protected

-Often, the system requires foreign accusers to prove that dumping is occurring in order for antidumping duties to be instated

2: Countervailing duties: a tariff imposed as a trade remedy to counteract foreign governments subsidizing their industries

-Governments wishing to impose countervailing duties must prove that there is a foreign subsidy being used to bolster a certain foreign industry, and that it is significantly harming the prospects of domestic producers

-The U.S. is currently placing countervailing duties on Canadian softwood lumber.

-----------------------

IMPORTANT ORGANIZATIONS AND TERMS

GATT- The general agreement on trades and tariffs: an effort to reduce international protectionism

The Uruguay Round- reduced tariffs by 40%, but failed to deal with European and Canadian agricultural subsidies (eventually, they ended quotas, but replaced them with Tariffs in a process called Tariffication)

WTO- World trade organization- it has 148 members, it is a global organization which deals with the rules of trade, and it endeavors to lower trade and non-trade barriers. It also includes a formal dispute settlement mechanism

Doha Round- tried to reduce agricultural subsidies

The Battle for Seattle- People protested that human, labour, and environmental rights were not being addressed by the WTO. Interestingly, 3rd world countries often argue against considering these in trade deals

MAI- Multilateral agreement on investment: similar to WTO, but for investments

Free trade Area- Goods and services may move freely among member countries, but each member nation still sets barriers against foreign imports on an individual basis (like NAFTA) PROBLEM: Certain Tariffs have grandfather clauses, and thus persist despite agreements.

Customs Union- A free trade area, but with a common set of barriers against foreign imports (like Mercosur: Brazil, Uruguay, Paraguay, and Argentina)

Common Market- A customs union in which factors of production (i.e., workers) may move freely among member nations (like the EU)

THAT'S ALMOST ALL!!!